Stock Seasonality in Python - A Tutorial

Normally I’d add this to my Python Tutorial page but sometimes these small scripts are better found (and indexed) by Google if they’re in their own post. After writing my article on Seasonal Trading and Investing Strategies, I decided to port Eric’s R code to Python.

While Eric’s code in R is very compact, the Python version feels more expressive and easier to deduce. I spent an hour or so trying to figure out the various methods that were called from the PerformanceAnalytics library and the ROC function from the xts library. As a machine learning guy, ROC means something completely different than the xts library method.

```import pandas as pd import numpy as np import yfinance as yf import matplotlib.pyplot as plt import datetime as dt

Get the Stock Ticker

tickers =‘NVDA’

Set the Start Date, Ending Date Is Today

start=dt.datetime(1970,1,1) end = dt.datetime.now()

Download Stock Data

assets=yf.download(tickers,start,end) #[‘Adj Close’]

Renaming to Humane Column Names

assets.rename(columns={‘Adj Close’: ‘Adj_Close’}, inplace=True)

Checking What the Data Looks Like

assets.head()

Compute Daily Returns Using Pandas Pct_change()

assets[‘daily_returns’] = assets[‘Adj_Close’].pct_change()

Skip First Row With Na

#assets = assets[‘daily_returns’][1:] assets = assets[1:]

Do a Plot to Check Time Series

plt.plot(assets[‘daily_returns’])

Break Time Series Into First and Second Half of the Year

first_half = assets[assets.index.month.isin([1,2,3,4,11,12])] second_half = assets[assets.index.month.isin([5,6,7,8,9,10])]

Check First Half Data

first_half.head()

Calculate the Cumulative Daily Returns for First Half of Year

first_half[‘FH_Culm_Return’] = (1 + first_half[‘daily_returns’]).cumprod() - 1

Plot First Half Data Transform for Sanity Check

plt.plot(first_half[‘FH_Culm_Return’])

Calculate the Cumulative Daily Returns for Second Half of Year

second_half[‘SH_Culm_Return’] = (1 + second_half[‘daily_returns’]).cumprod() - 1

Plot First Half Data Transform for Sanity Check

plt.plot(second_half[‘SH_Culm_Return’])

Prepare Series for Concatentation

s1 = first_half[‘FH_Culm_Return’] s2 = second_half[‘SH_Culm_Return’]

Fill NaN With Last Value

s1.fillna(method=‘ffill’, inplace=True) s2.fillna(method=‘ffill’, inplace=True)

Concat Series Together and Set to Out Df

out = pd.concat([s1, s2], axis=1)

Fill NaN With Last Value

out.fillna(method =‘ffill’, inplace=True) out

This Step Is Optional, You Can Resample to 1 Month or Leave As-Is

#out = out.resample(‘1M’).asfreq().ffill()

Plot the Final Results of the Two Series.

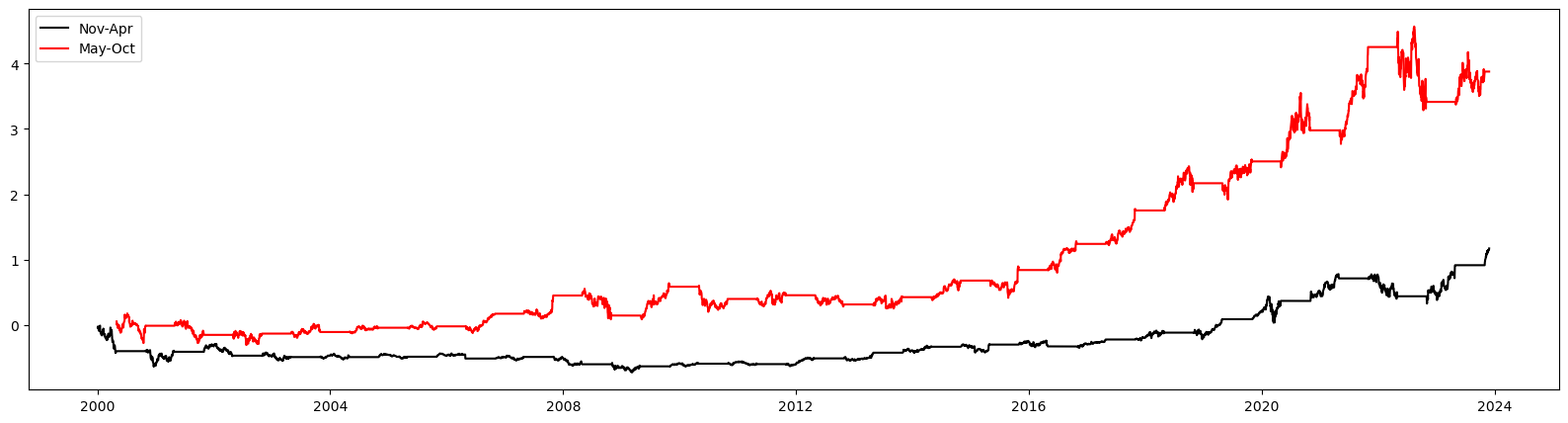

plt.figure(figsize=(20,5)) plt.title(tickers+” Seasonal Performance”) plt.xlabel(‘Year’) plt.ylabel(‘Culmulative Perf’) plt.plot(out.FH_Culm_Return, color = “black”, label=‘Nov-Apr’) plt.plot(out.SH_Culm_Return, color = “red”, label=‘May-Oct’) plt.legend() plt.show() ```

I did spend time on Stackoverflow piecing together some data munging requirements. While you can do anything in Python, R’s handling of data was a bit more elegant. Still, I prefer Python over R any day.

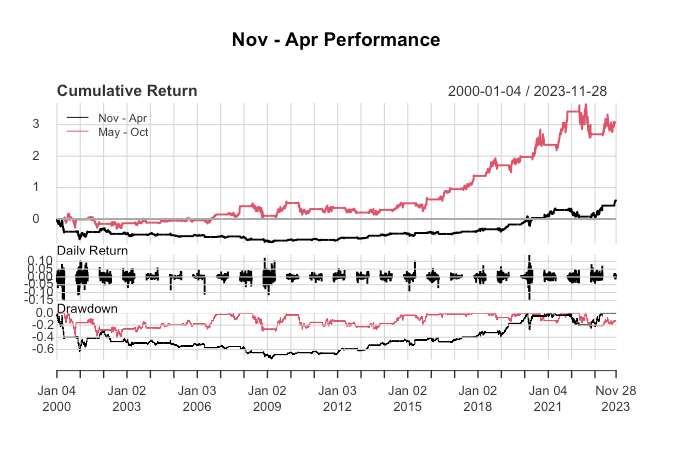

This is what the MSFT looks like from the year 2000 on in R.

MSFT Seasonality in R

MSFT Seasonality in R

And this is what MSFT looks like from the year 2000 in Python.

MSFT Seasonality in Python

MSFT Seasonality in Python

Granted I need to add the drawdown and the daily return part to the Python code, but the hard nut has been cracked.